When risk reasserts itself: Understanding the capital stack

The concept of the capital stack is a familiar one to most professional investors. It describes where an investment might sit within a capital structure – typically as debt or equity – and determines the order in which investors are paid or recoup their capital.

While often discussed in theory, the practical implications of capital stack positioning can be overlooked. As volatility, inflation and economic uncertainty continue to test markets, investors are being encouraged to take a closer look at where their investments sit in the capital stack – particularly within credit investments – and to ensure they fully understand the risk profile attached to each position.

Chris Paton, Chief Investment Officer of Australian alternative asset manager La Trobe Financial, said that clarity around capital stack positions is an important part of informed portfolio construction.

“Understanding the structure of any investment – not just its headline return – is critical,” Mr Paton said. “Investors want to avoid unexpected outcomes that can arise when the risk characteristics of an investment are not fully understood.”

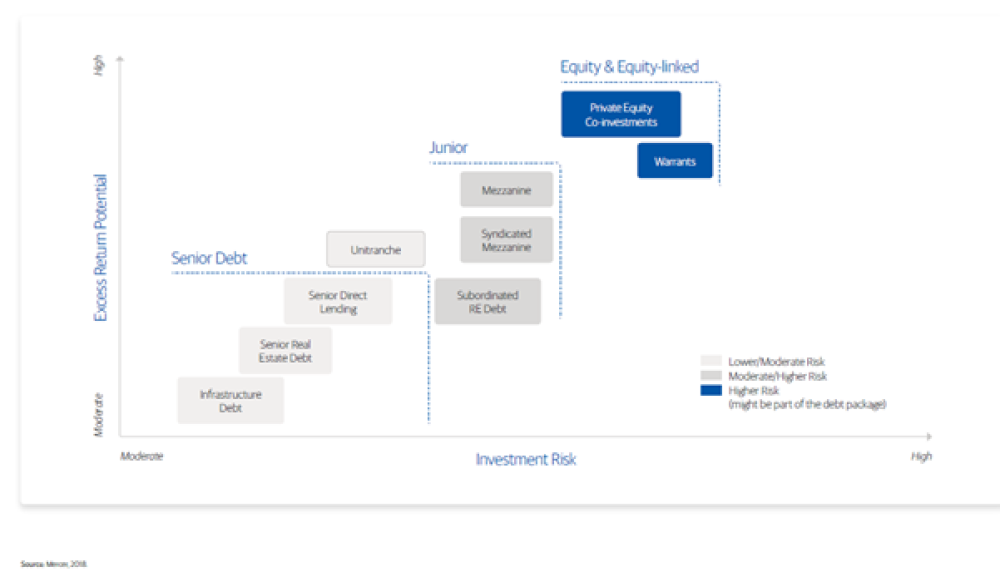

What the capital stack represents

While structures can vary, a simplified illustration typically includes three broad layers:

Senior secured debt

This includes instruments such as first registered mortgages over property or first‑ranking security over company assets. These positions have the highest priority in the capital stack and are therefore the first to be repaid if an asset is sold or a borrower defaults.

Mezzanine / Junior debt

This layer can include second mortgages, second‑lien loans, unsecured facilities or shareholder loans. These investors are repaid after senior secured lenders and typically receive higher returns to compensate for the additional risk.

Equity

Equity exposures, such as direct company ownership or private equity investments, sit further along the capital stack. Equity holders participate in upside but are also the first to absorb losses if performance deteriorates.

Put another way, the capital stack defines how losses – and recoveries – are distributed when conditions deteriorate, with equity absorbing losses first and senior secured lenders having the strongest claim on underlying assets.

“If you’re allocating capital across different asset types, understanding where each investment sits in the capital stack helps you better assess how it may behave under stress,” Mr Paton said.

The Capital Stack: Senior, Mezzanine, and Equity Positions

Why capital stack awareness matters

Mr Paton said investors should not assume that investments labelled “credit” or “income” necessarily carry the same risk characteristics.

“When you look closely at portfolios, you may find that some include allocations to equity or equity‑like exposures alongside traditional credit,” he said. “That isn’t inherently good or bad – but it does change the risk profile, particularly during periods of market dislocation.”

He added that transparency around portfolio composition was essential for investors seeking to understand how returns are generated and where vulnerabilities may lie.

“For investors, the key questions are about awareness and alignment,” Mr Paton said. “What proportion of a portfolio sits in senior secured positions? How much is subordinated or equity‑like? And does that align with the role the investment is intended to play within the broader portfolio?”

Different layers of the capital stack can serve different objectives. Equity may suit investors seeking long‑term growth and willing to accept volatility, while credit investments may appeal to those prioritising income. The appropriate mix will vary depending on investor goals, time horizons and risk tolerance.

Capital structure during periods of stress

Periods of market stress tend to highlight the practical importance of capital structure. According to Mr Paton, outcomes during these periods are often shaped by both capital stack positioning and the quality of the underlying assets.

“Investors across the capital stack are exposed if the underlying borrower or asset underperforms,” he said. “That’s why due diligence on asset quality and underwriting standards matters alongside structural considerations. It’s all about alignment, and giving yourself the best chances of achieving your investment goals”

For advisers and investors assessing private credit allocations, Mr Paton said discipline during both strong and weak market conditions was critical.

“It’s easy to focus on attractive target returns during favourable conditions,” he said. “But investors should also consider how a portfolio is likely to perform when conditions are less benign, and whether the structure and transparency of the strategy support informed decision‑making.”

Key considerations for investors assessing private credit or alternative strategies include:

- the manager’s investable universe and mandate

- the positioning of underlying assets within the capital stack

- transparency around portfolio construction, valuation and risk management

Mr Paton said that clear disclosure and consistency of approach were particularly important for investors relying on these strategies for income or capital preservation.

“Ultimately, understanding where your investment sits in the capital stack – and how that aligns with your objectives – is fundamental,” he said. “Transparency allows investors to make informed choices, regardless of the strategy they pursue.”

This is the final article in a three‑part series on the role of private credit when risk reasserts itself. The first two articles examined inflation‑responsive portfolios and income preservation during periods of volatility.

Content Partnership sponsored by La Trobe Financial

Any financial product advice is general only and has been prepared without considering your objectives, financial situation or needs. La Trobe Financial Asset Management Limited ACN 007 332 363 Australian Financial Services Licence No. 222213.

And yet Innocent Advisers will still be belted for the biggest CSLR Adviser Theft Levies to pay for every other…

I appreciate that we are stuck with the Government thievery that is the CSLR. The constant (and fair) argument from…

CLSR was meant to be the ‘last resort’, not the GoTo funding model that would unfairly burden honest business operators…

Unregulated MISs the base problem. Yet MIS remain out of CSLR ? And MIS remain largely Unregulated. WTF Corrupt Canberra

Exactly