Stark differences in private credit investment costs

New analysis from research and ratings house, Morningstar has painted a complex picture of private credit investment in Australia suggesting that private asset-oriented structures cost considerably more relative to their equivalent broad-based universe.

The Morningstar manager research fund pointed to recent headlines around redemptions and gating and have suggested that they have sharpened investors’ focus on structures “that look familiar on the surface but behave very differently from traditional managed funds”.

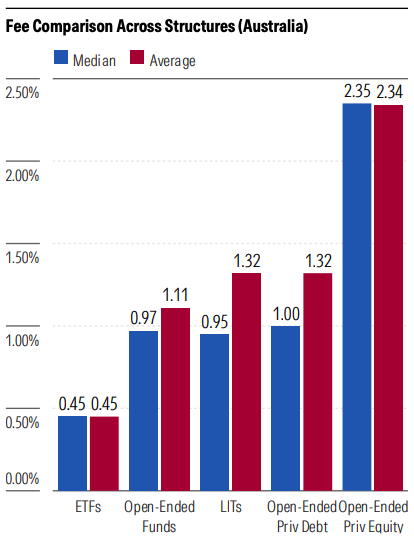

In doing so, the Morningstar team have published a fee comparison across structures which provides a stark contrast between the cost of exchange traded funds (ETFs) and open-ended private equity.

The research, Demystifying Semiliquid Fund Structures – an Asia-Pacific Perspective draws some pointed conclusions, not least noting drawing comparisons between India, Hong Kong, Singapore, Japan and Australia and noting while the other jurisdictions have limits on investor eligibility, “by contrast, Australia is notably laissez-faire”.

“…while there are income and asset tests to distinguish between regular and sophisticated investors – and the latter investor class can access less-regulated, complex investments – access to numerous private asset products is available to individual retail investors via vehicles such as evergreen funds and Licensed Investment Vehicles (LIVs),” it said.

However, it is on the question of fees that the Morningstar research is most pointed, noting that “unlike traditional open-ended vehicles for liquid asset classes, semiliquid fee structures tend to be heterogeneous and complex in nature; they also tend to be more expensive. Other than base management fees, products may charge incentive fees or carried interest subject to hurdles, high-water marks, and/or clawback provisions. They may also include fixed upfront and fixed annual fees; in Japan, we have observed such fees as high as US$3,000 and US$30,000, respectively; quite the cost!”

“Withdrawal fees are another element to look out for; they can be set very high to specifically disincentivize frequent redemptions; we have seen these as high as 5%.”

“Among fund structures, master-feeder funds warrant particular caution; they may incur multilayered management fees. Coupled with incentive and distribution fees, the total level of fee leakage by investors in such structures can be substantial.

“Private credit managers may earn generous origination fees (and default fees) from their borrowers, which are often fully passed on to investors. However, in markets such as Australia, managers may retain a portion of such fees without having to disclose their quantum to investors. Separate from presenting potential conflicts, origination fee retention enables managers to reduce disclosed management fees artificially; investors may be attracted to a well-priced fund, unaware that the income they’d otherwise receive is being retained by the manager.

“Using the Australian market as an example, it’s evident that private asset-oriented structures cost considerably more relative to their equivalent broad-based universe. For example, LITs, which are private credit-focused, typically cost more than twice as much as ETFs. Similarly, private debt and private equity evergreen vehicles are also more expensive versus open-ended funds, especially private equity,” the Morningstar research said.

Is BID not a thing? Is the trusted adviser based on member retention within the IFS network? What a joke.

Trustees going well hey. How much CSLR are these dodgy Super Trustees paying ? None of course, just whack Innoncent…

Ridiculous, once again the industry funds are losing so much money they need to grasp at straws to say the…

With any profession there always will be rotten apples in the barrel until they are discovered/ dealt with and prosecuted.…

Imagine if we had "Bank Aligned Adviser" But apparently this is different...... I wonder if they take the IFS Trusted…