Private debt a comfortable option in diversified portfolios

Recommending that clients make an allocation to private debt is still not at the top of the list for many financial advisers, yet it probably sits more comfortably in a well-diversified portfolio than many Real Estate Investment Trusts (REITs).

At least part of the issue for financial advisers is the perception that private debt is a comparatively new allocation when, in fact, it is an allocation the banks have been providing for decades.

And the bottom line is that Australian legal history makes private debt allocations a safer investment than in many other jurisdictions because of this nation’s corporate insolvency laws which have been derived from those in the UK which impose specific obligations on borrowers.

Thus, private debt allocations on the part of advice clients, particularly high net worths, have been increasing, notwithstanding the volatility generated by COVID-19 and geopolitical events over the past four years.

Metrics Credit Partners has become a lead player in the private debt space not least because it is also the largest non-bank lender to the commercial real estate sector.

Metrics managing partner, Andrew Lockhart well understands the misunderstanding that private debt represents a comparatively new allocation, but suggests that in reality it is an excellent portfolio diversifier.

“In terms of investor allocation, it’s about diversification and I think Australia presents a pretty attractive investment market and opportunity,” he said.

Looking at retail investor attitudes to private debt, Lockhart is pragmatic about the need to generate understanding of the asset class in the context of the more traditional investments with which they are more familiar.

“People are very familiar with public market equities, public market bonds and the like and so when they start to move into what they perceive as a new asset class, even though it’s an asset class the banks have been providing for many, many years there is hesitance,” he said.

“It takes time to educate people and demonstrate the track record of performance and the like.”

He said the messaging for private clients and retail investors about private debt came down to two things:

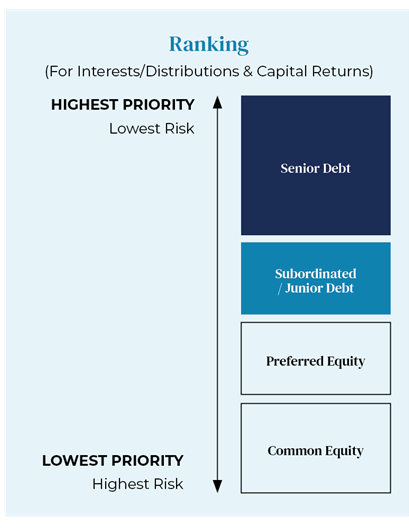

(1). It is around the stability of capital and where you sit in the capital structure. Senior secured debt ranks in priority to shareholder equity and any unsecured creditors. So when you’ve got a secured debt you’ve got security held over the borrower along with controls and covenants – all of the things designed to protect a lender’s capital to mitigate potential risk of loss.

(2). Investors are looking for income. Income from private debt can span a very broad market and so at one end of the risk spectrum it can provide an alternative to defensive traditional fixed income and, at the other end of the spectrum, it can provide returns that exceed what they may obtain through equities but for lower risk.

“It allows the adviser to look at what the client’s return objective is, discuss their risk tolerance and then look at how they can access the market. The liquidity of the chosen vehicle is important if the investor’s circumstances change,” Lockhart said.

“It is really important that a manager has a range of different funds and different vehicles that can cater to a client’s needs because the market is not homogenous and investors requirements are not the same.”

“We see a very broad set of opportunities in the market and we can structure terms and conditions and pricing with our borrowers that leads to an outcome for our investors,” Lockhart said. “And one of the things that investors need to consider in terms of accessing private credit is the need to invest via well-diversified portfolios – it’s not so much about industry risk it’s about individual counter-party credit risk.”

“Importantly, what an investor needs to look at is just ensuring that the exposure to any one individual borrower or investment isn’t so large that it may adversely impact their capital.

“You would expect that there would be ups and downs in any market but importantly, if you are in a well-diversified portfolio of debt, you are at a much lower risk of loss than you would be in other asset class, particularly some more concentrated equities portfolios,” Lockhart said.

To learn more about Metrics Credit Partners, visit www.metrics.com.au

Content Partnership sponsored by Metrics Credit Partners

SMSF Limited Advice licensing = yet another stupendous Govt Disaster. It has certainly proved to Accountants that ASIC & Govts…

Platforms unfairly blocking innocent Advisers?

Right, so we (advisers) ended up remunerating a bunch of Canberra Bureaucrats who never lost any money? No wonder they…

I note Treasury are yet to make submissions public. They are known for doing this as transparency is not their…

And every input (except the FSC) wants MIS as front line CSLR levy payers. Plus: MISPlatforms Research Responsible Entities Super…