Global REITs: Mispriced in Plain Sight

Global real estate investment trusts (REITs) are currently significantly mis-priced which means there are genuine opportunities for investors will to look beyond the prevailing volatility, according to Dexus Head of Real Estate Securities, Mark Mazzarella CFA.

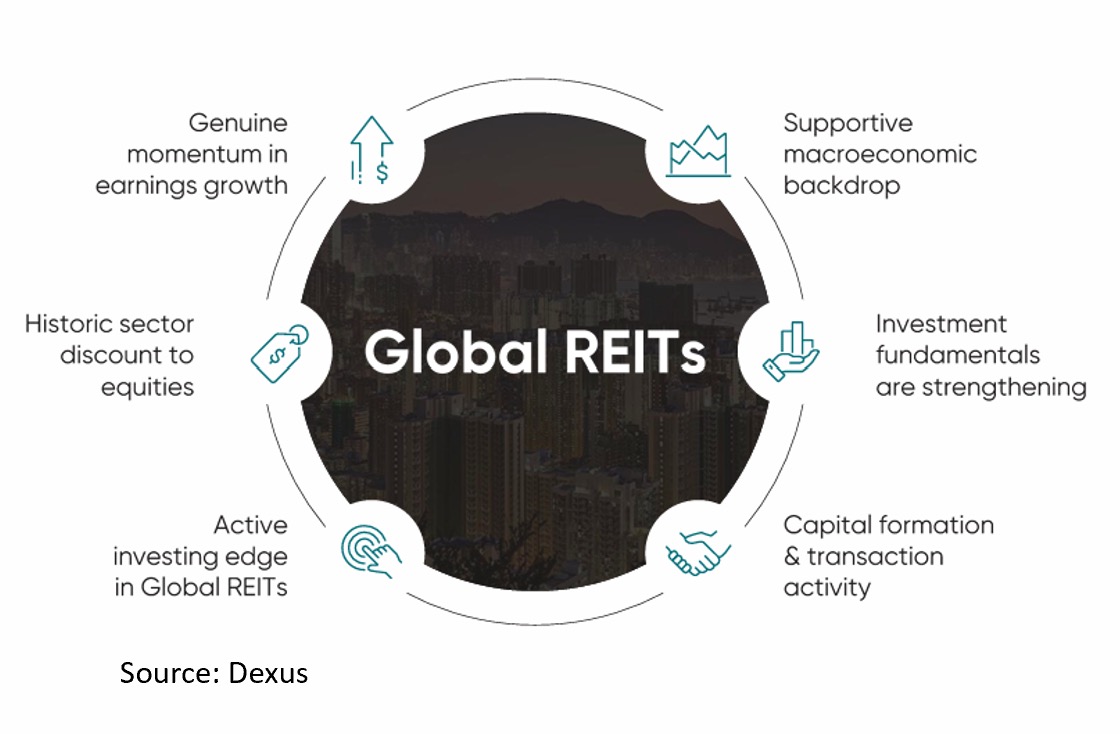

Discussing the issue at the recent IMAP Portfolio Management Conference, Mazzarella said Global REITs are trading at rare, wide valuation discounts relative to global equities and below their net asset values (NAV). Despite strengthening operational fundamentals — including positive rent growth and constrained new supply — REITs have underperformed general equities for four consecutive years. On both a “price to cashflow” and “price to book” basis, the discounts are historically wide, signalling that a sector backed by tangible, income-generating assets remains materially undervalued.

From a top-down perspective, Mazzarella points to the stabilisation of interest rates in most developed markets post-COVID as a key positive. This has normalised the cost of capital for real estate investment, particularly in markets like the United States, making the sector’s economics more attractive. However, it is the bottom-up dynamics that he finds most compelling. The cost of constructing or developing new property has risen exponentially since COVID, a trend likely to continue, making it extremely difficult to bring new supply to market. This supply constraint is a global theme across the built-form market, with only data centres having managed to add meaningful new inventory in recent years.

This supply/demand imbalance, combined with the nature of real estate earnings — driven by rents indexed to inflation or fixed annually — creates a powerful engine for bottom-line growth. The Dexus Global REIT Fund has achieved a weighted average three-year earnings compound annual growth rate (CAGR) of around 6–7 per cent, demonstrating the resilience and consistency of the sector even through periods of broader market uncertainty.

On portfolio diversification, Mazzarella highlights that many major equity indices are heavily concentrated in the “Magnificent 7” — Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla — which collectively accounted for approximately 30–35 per cent of the S&P 500’s market capitalisation as of early 2026. REITs, by contrast, offer a diversified, liquid, global exposure to real assets without the valuation excess of these technology giants. For investors seeking attractive returns from assets that are not overvalued, Global REITs present a compelling alternative.

Beyond the traditional real estate sectors of retail, office, and industrial — which are closely tied to the business cycle — Mazzarella is particularly excited about sub-sectors that operate independently of economic cycles.

Seniors living stands out as a key opportunity, driven by rapidly ageing populations in developed markets creating sustained demand that cannot be suppressed.

Assisted living similarly benefits from a structural supply/demand imbalance, offering some of the strongest rental tension seen anywhere in real assets.

Data centres are also identified as a structural opportunity, benefitting from the tailwinds of AI and digital infrastructure growth. However, Mazzarella urges caution, noting that data centres carry significant obsolescence risk — as technology evolves rapidly, facilities can become unable to support modern high-density computing hardware within just a few years of construction. Dexus therefore takes a selective approach, focusing on pre-committed or de-risked assets, and investing in established operators such as Equinix.

Looking ahead, Mazzarella remains bullish on Global REITs despite the current period of macro uncertainty and volatility. He notes that transaction evidence reveals implied yields and capitalisation rates in the listed market are trading at discounts of 20–30 per cent or more — a clear signal of mispricing. For Dexus, the current mispricing in Global REITs makes a compelling case for investors to include an allocation to the sector in their portfolios.

To watch these sessions in full and earn CPD Click here

So Senator O'Neill can see how these government bodies failed to pick up the scam, yet it is advisers who…

Why doesn't ASIC all out these "profit share" arrangements between insurers and super fund trustees, which obviously fly in the…

Of course ASIC don't name and shame their best buddies ISF's. That's for lowly bottom dwellers Financial Advisers to be…

Of course ASIC dont name and shame their best buddies ISF's. That's for lowly bottom dwellers Financial Advisers to be…

Are they saying there are potentially other Shields and First Guardians out there but it’s someone else’s job to analyse…