Consumer discretionary to suffer from rate hike aftershocks

The consumer discretionary sector has been singled out by long-only fund manager, Datt Capital, as one likely to suffer most from a potential third consecutive rate hike by the Reserve Bank of Australia (RBA).

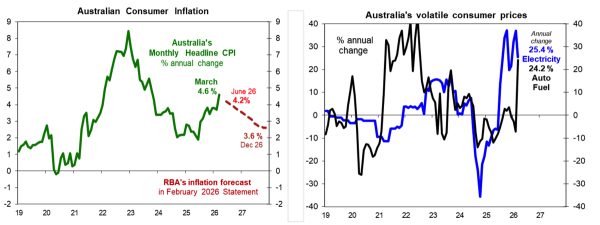

The assessment from Chief Investment Officer, Emanuel Datt, comes as the latest Australian Bureau of Statistics (ABS) data release confirmed headline Consumer Price Index (CPI) jumped by 4.6 per cent in the 12 months till March – 0.9 per cent surge from February’s figures.

Datt said this all but confirms that the RBA “has no room” to pause its tightening cycle and investors preparing for a temporary “risk-off moment” will be sorely mistaken.

“The instinctive response to a tightening cycle is to reduce risk broadly,” Datt said.

“That’s understandable, but it’s imprecise. Rate hikes don’t transmit evenly across the economy. The analytical discipline required right now is understanding how rate changes impact each sector and identifying which businesses have the earnings quality to absorb sustained pressure.

“The transmission mechanism is direct. Higher mortgage repayments reduce the share of household income available for non-essential spending.

“For Australian households still carrying elevated debt levels, each successive hike compounds the effect of the last. If the May hike proceeds and consumer confidence data keeps deteriorating, investors should expect earnings revisions across the sector.

“The defensive label for consumer staples is partially correct but incomplete. The real risk for staples businesses isn’t revenue loss – the demand for essential goods is relatively inelastic. It’s margin compression.

“Input costs across energy, logistics, and raw materials have risen materially. Passing those through is constrained by competitive pricing and the growing prevalence of private label alternatives. The defensive label doesn’t protect against a structural cost squeeze.”

Datt noted that industrials are also in the same camp as consumer discretionary, while flagging areas that aren’t reliant on domestic rate movements – such as upstream energy producers, oil (fuelled further by the conflict in the Middle East) and gold – as attractive opportunities amid current market conditions.

“Industrials are being hit from both directions simultaneously. On the demand side, higher rates slow construction and infrastructure activity and on the cost side, energy and financing costs rise directly,” he said.

“For capital-intensive businesses on fixed-price project contracts, that timing mismatch between rising input costs and locked-in pricing creates earnings risk that often isn’t visible until results season.

“For upstream producers, the domestic cash rate is largely a secondary variable. Revenue is driven by commodity prices set in global markets. The ABS data makes this visible in real terms — diesel rose 41 per cent between February and March alone, from 181 cents to 256 cents per litre.

“For producers with low extraction costs, that price environment flows directly into revenue. Their cost base doesn’t rise in proportion to revenue, which means free cash flow generation at elevated commodity prices can be substantial.

“It’s important to distinguish within the sector. Value doesn’t accrue evenly across the energy value chain. Upstream producers with low production costs and strong reserve bases are best positioned.

“Downstream operators and refiners face structurally thinner and more volatile margins. That distinction matters for portfolio construction.

“Historically, gold performs well during periods of monetary policy uncertainty and sustained above-target inflation. If the RBA hikes in May and inflation data remains sticky through mid-2026, the conditions supporting gold prices remain firmly in place.”

On technology, Datt highlighted the “common characteristics” that would best support businesses during the next wave of tougher market conditions: “their earnings are driven by factors independent of domestic consumer spending; they carry pricing power that doesn’t depend on volume growth; and their balance sheets don’t require refinancing at materially higher rates”.

“High-growth, pre-profitability companies are mechanically sensitive to rising discount rates, and that’s well understood. But profitable technology businesses with recurring revenue, low capital requirements, and minimal debt are in a structurally different position.

“Their cost base doesn’t rise materially when rates increase. Their customers are typically businesses, not rate-sensitive households, and the productivity case for enterprise software doesn’t change with the cash rate.

“Small companies are frequently under-researched relative to large caps, which creates pricing inefficiencies that primary research can identify before the broader market catches up. In a rate environment where consensus positioning is being rapidly repriced, that information advantage is more valuable, not less.

“At 4.6 per cent headline CPI, the real return on a term deposit running at 4 to 4.5 per cent is negative before tax. An absolute return strategy targeting positive real returns across the cycle should become a real consideration for investors.”

Meanwhile, financial advisers are fully accountable for tax outcomes relating to advice and still cannot access the ATO portal. Accountability…

PJ is usually too busy organising his next conference to attend, or sending by accidental emails to members, .or even…

Unless I’m misinterpreting this this ‘bonus’ is just giving the member what they technically already own as I’m assuming this…

Let’s see the new AIOFP white label platform real soon. As long as it’s price competitive and works, with no…

YES! you idiots. Of course it should. Then can we sue the government for forcing the closure of small /…