CPI prompts rate rise predictions

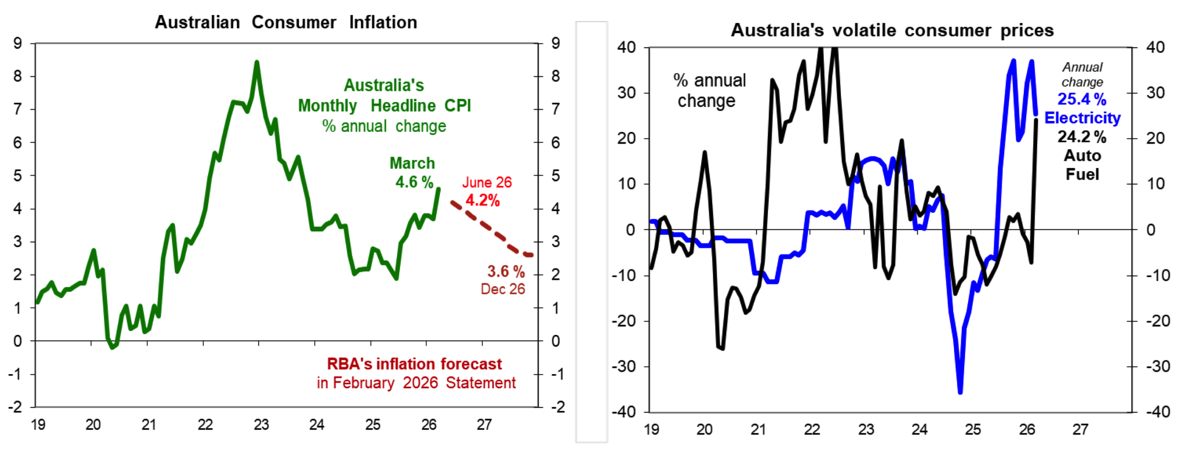

A broad cross-section of Australian market economists are inking in another 0.25% interest rate rise next month in the wake of yesterday’s March quarter rise in the consumer price index (CPI) to 4.6%.

The tone of sentiment was set by MLC Senior Economist, Bob Cunneen who said it reflected the dramatic impact of the Iran War on energy prices and represented “a dramatic surge compared to February’s 3.7% annual result”.

Cunneen’s assessment was similar to that of HSBC chief economist, Paul Bloxham who said the main message from the CPI figures was a confirmation that, as expected, core inflation is too high, and well above the RBA’s target in the first quarter.

“Although the headline CPI was a bit weaker than the market expected, at 4.6% y-o-y in March, versus an expected 4.8%, the key indicator that the RBA focuses on, the quarterly trimmed mean was in line with the market expectation over the year, at 3.5%,” he said.

Bloxham said that, for the Reserve Bank of Australia (RBA), the figures supported the case for a further rate hike in May.

“The key to whether the RBA lifts rates again, after the expected move in May to 4.35%, will be how quickly economic activity and the jobs market weaken over the coming period,” he said.

“If the sharp fall in business and consumer sentiment that occurred in the latest readings is a good guide, then the economy is weakening quickly and we expect this to prevent the RBA from lifting rates beyond a cash rate of 4.35%. However, if activity and the jobs market prove to be more robust than we expect, the RBA could lift its cash rate even further.”

Colter Bay Capital chief executive, Mark Wang was not as certain about the RBA imposing a rate hike.

“The immediate reaction is to assume this locks in another RBA hike, but that’s not a given,” Wang said.

“Australia is heavily exposed to housing, and higher rates flow straight into mortgage repayments rather than productive investment, which changes how the tightening cycle feeds through the economy.

“Each additional basis point pulls spending away from households and small businesses and into debt servicing, and at some point that becomes the bigger risk, particularly when much of the current pressure is coming from imported energy costs that monetary policy can’t meaningfully influence. Sentiment is usually the first thing to turn, and it is already showing signs of strain.”

ASIC have ignored property marketers flogging properties to SMSF's for years, this won't change because of the budget. All of…

FAAAAAAAAAAAAAAAAA sound like an ISF mouthpiece. ASIC need to stop SMSF Property spruikers, I have handed them a case for…

Seriously FAAA? How about you focus on the detriment of CGT and negative gearing changes to share portfolios and stay…

No - no carve outs for accountants. If they want to provide financial advice, they can jump through all the…

Many accountants already provide bucket loads of illegal AFSL Super / SMSF Advice and ASIC do nothing about it. Accountants…