Gutting of life/risk advice again hits premium sales

The decimation of the life/risk adviser distribution channel sits behind yet more negative numbers for life insurance sales, according to the Dexx&r managing director, Mark Kachor.

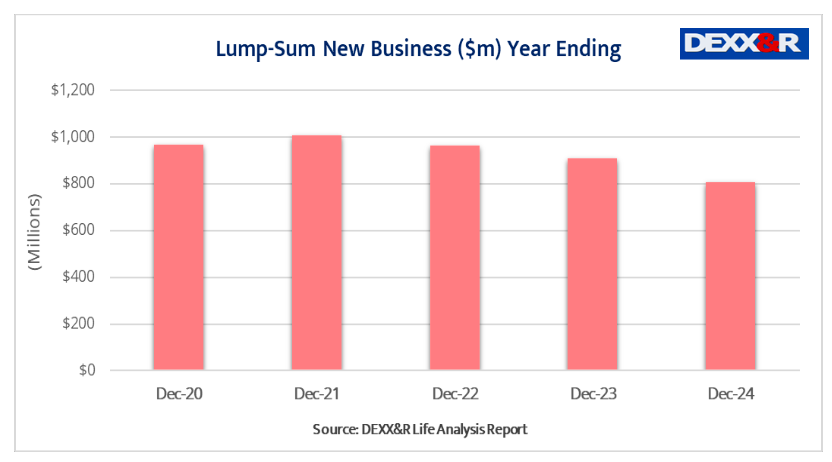

Specialist life/risk research house, Dexx&r released its latest Life Analysis Report based on data for the 12 months ending December, 2024, and the bottom line was that individual risk new premiums were down 18.5% for the period to $1.11 billion.

It said that total risk in-force premium decreased by 1.7% over the 12 months down from the $16.5 billion recorded at December 2023 to $16.2 billion at December, 2024.

Commenting on the data, Kachor said that the most important factor impacting the life/risk data was the exit of specialist life/risk advisers.

“It’s a distribution issue,” he said. “Over the last few years we have seen an exodus of life/risk advisers; many of the old and bold and most experienced have left the industry and moved on.”

He said the negative data had little to do with the quality of the products being taken to market by the life insurers in circumstances where death cover, for instance, had rarely been cheaper.

The Dexx&r data also pointed to the fact that Disability Income new business decreased by 33.3% to $301 million over the year, down from $451 million in the prior corresponding period.

It said that the Dexx&r attrition rate for disability income business increased to 11.4% in December, up from 10.9% a year earlier.

The analysis said that the discontinuances had continued to climb from the 9.1% low recorded in December 2020 immediately prior to the release of a new range of disability income products following the Australian Prudential Regulation Authority’s (APRA’s) intervention and the release of new products in 2021.

In the group risk market dominated by superannuation fund default cover, the Dexx&r data actually pointed to a modest 0.3% increase over the 12 month period, noting that while the Protecting Your Super legislation had meant fewer super fund members with default cover, total premium received had continued to increase as a result of the re-pricing of existing benefits”.

LOL - the current number isn't the floor. It's just a pause as more declines are incoming tks to insane…

Someone is fudging the numbers on the number of active advisers available to provide advice! While there may be in…

When they leave a licensee they come off the list. When they commence with a new one they come back…

You have a reversal in number. 15203 and another 15023…

How does an adviser shifting licensees add to a new adviser list ?