Building resilient portfolios is key

Investors are increasingly asking whether inflation will remain higher for longer, whether geopolitical risk has become a permanent investment consideration, and how the AI investment boom should influence portfolio construction. Cameron Harrison’s David Clark says the answer to all three questions is shaping how the firm is thinking about long-term capital allocation.

Three Key Takeaways

- Inflation is looking structural, not temporary. The global rebuild of supply chains, energy systems, defence, and AI infrastructure is competing for the same raw materials, energy, and capital, keeping steady pressure on prices.

- RBA headwinds persist. Expected rate cuts turned into increases, lifting the cash rate to 4.35%. Stronger collective bargaining power has seen wage increases rise above a level consistent with 2-3% inflation, creating further headaches for the RBA.

- Resilience is not just diversification. Cameron Harrison is building portfolios to perform across a range of key themes and outcomes rather than betting on any single position.

Three forces shaped investment markets in the year to 30 June 2026: geopolitical risk, stubbornly high inflation, and an accelerating boom in artificial intelligence spending. Together, they point to a world that is noisier, more contested, and more inflationary than the one investors grew comfortable with over the past decade.

Australia’s economic performance improved as RBA cash rates fell in the first half of the year stoking housing and consumer activity, snapping a streak of eight consecutive quarters of negative per capita GDP growth to record GDP growth in the mid-2% range. However, better remains a long way from good: even this meagre level of economic activity proved too much in the face of weak productivity, and inflation quickly reversed course.

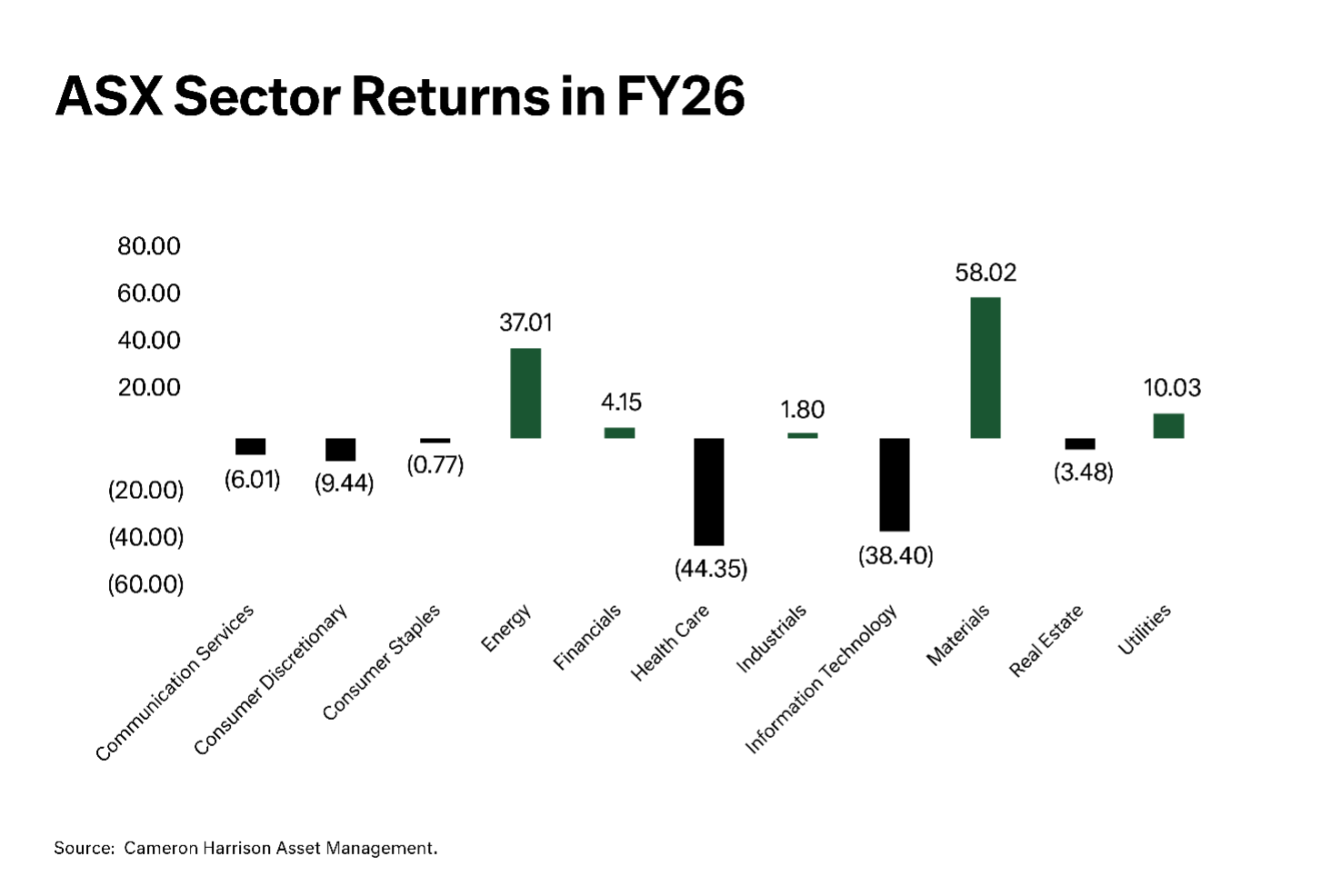

The domestic equity market reflected this underlying weakness with returns coming from a narrow set of winners, chiefly gold and resources, rather than any broad economic strength, with six of eleven sectors trailing inflation.

Sticky Inflation & the RBA

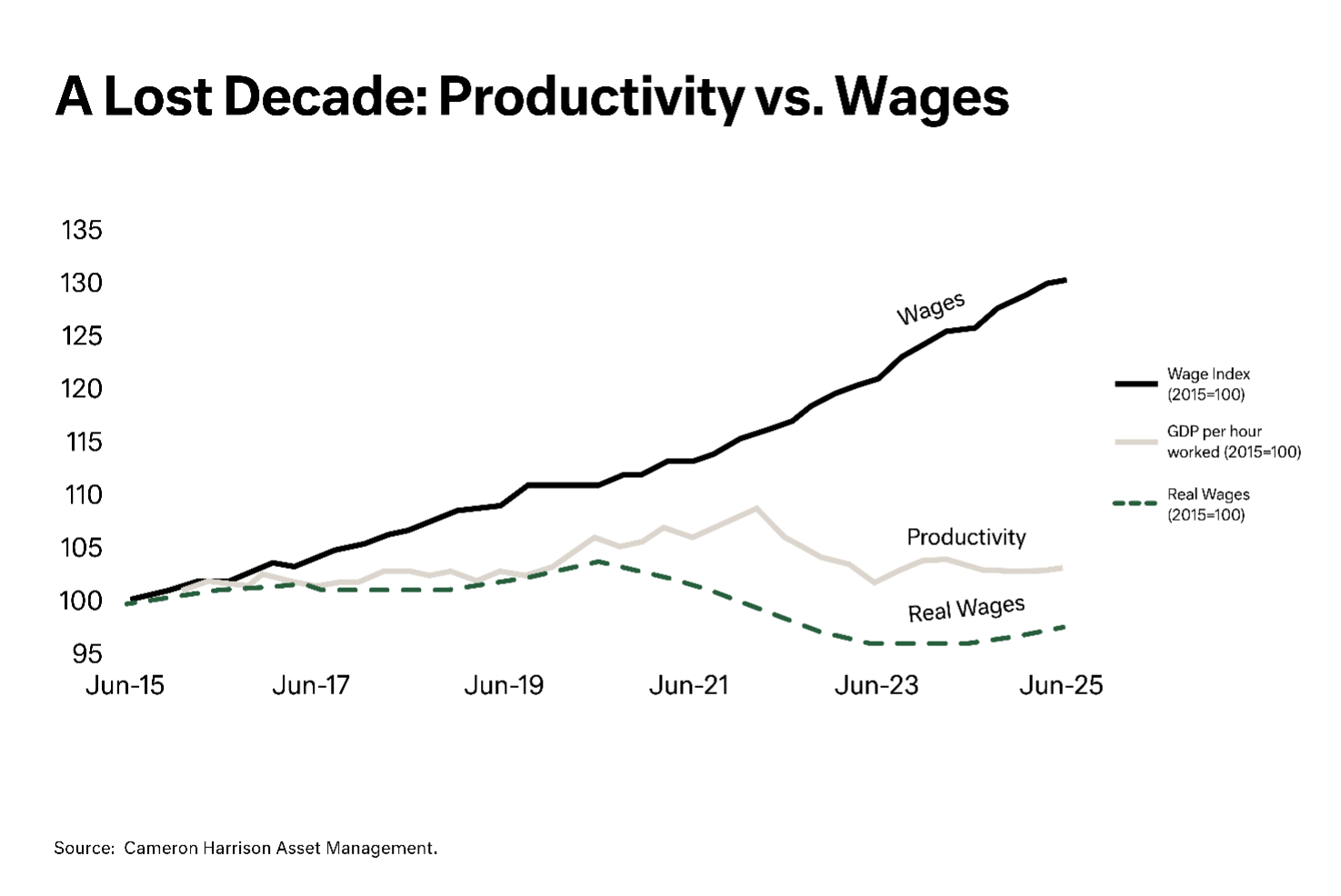

Sticky inflation saw the RBA’s cash rate expectations swing dramatically over the year from multiple projected cuts toward 3.10% to three increases instead, lifting the cash rate to its current setting of 4.35%, with a further move toward 4.6% anticipated. The challenge for the RBA has been a lack of productivity gains over the last decade, which has seen wage inflation transmitted into higher inflation. When you cannot do things more efficiently, wage growth flows directly into prices rather than prosperity. In the absence of a weaker employment market or improved productivity, inflation is likely to remain a problem for the RBA.

A Fragile World: Geopolitics, Supply Chains & AI Booms

The year’s sharpest jolt came from the conflict between Iran, Israel, and the United States. Oil jumped from around US$60 a barrel to nearly US$120 before settling back to where it started. With roughly 20% of global oil supply passing through the Strait of Hormuz, the episode was a reminder that supply chains built for efficiency, not resilience, remain acutely exposed to geopolitical shocks.

The response to that fragility, re-shoring production and rebuilding defence capability, will demand enormous investment. Decades of underspending are now being reversed, and that reversal carries a price.

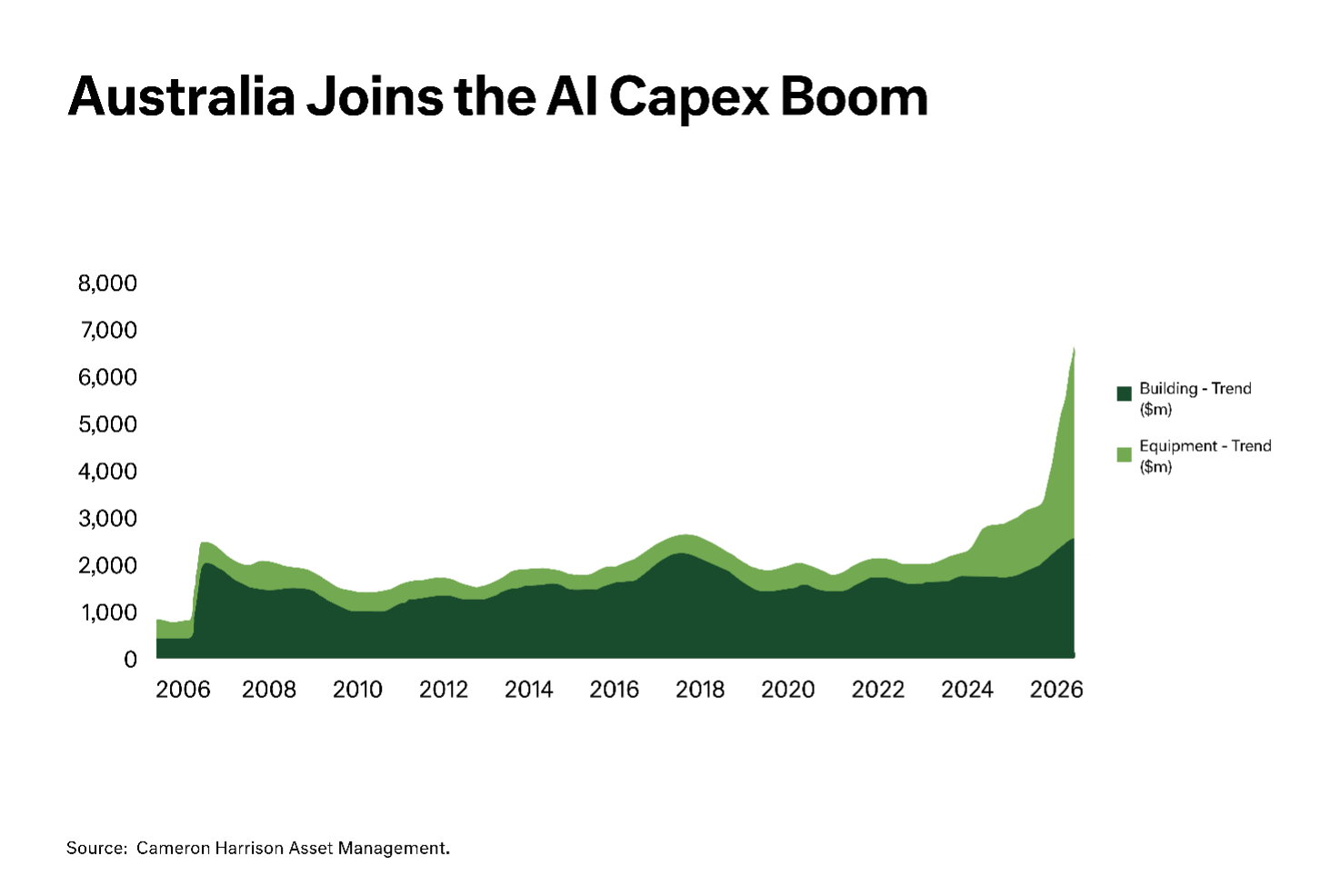

Australia has joined the global rush to build AI infrastructure. Investment in the telecommunications and IT sector, which ran at roughly $2 billion a year for two decades, has climbed above $7 billion, echoing the surge seen in the United States on a smaller scale.

Whether these data centres deliver lasting economic benefit is still an open question. They employ few people and import most of their components. What is not in doubt is their appetite for energy, construction, and raw materials.

Supply-chain resilience, the green energy transition, AI infrastructure, and defence all draw on the same finite pool of raw materials, energy, and capital. That competition is a structural support for inflation, and it helps explain why prices are proving so difficult to return to central bank targets. This is the backdrop against which Cameron Harrison positions portfolios.

What It Means for Portfolios

Resilience today means more than simple diversification. Cameron Harrison builds portfolios around four pillars: holdings with inflation-linked revenues, businesses positioned to benefit from the capital-expenditure cycle, geopolitical hedges, and income-stabilising assets delivering attractive real returns. Many holdings serve more than one purpose, but the aim is consistent: a portfolio that can perform across scenarios rather than one that depends on a single outcome.

In broad terms, that thinking plays out as follows.

- Australian equities. We are carrying our lowest weighting to Australian shares in Cameron Harrison’s history, with no near-term plans to lift it. The local market’s gains were narrow, driven by gold and resources rather than any broad improvement, and most sectors failed to keep pace with inflation. Where we do invest locally, we favour businesses at the start of the supply chain and those able to pass rising costs through to customers.

- Global equities. We hold offshore shares more heavily than domestic ones, reflecting stronger productivity, earnings, and a far wider opportunity set. The build-out of AI, energy, water, and defence infrastructure is a particular focus, complemented by a meaningful technology exposure.

- Interest income. Yields on high-quality interest income are at their highest in a decade, an attractive return for the lowest-risk part of a portfolio. We remain comfortably weighted here, favouring structures that offer both income and protection should rates rise further.

- Currency. With the Australian dollar around US$0.72, which we regard as broadly fair value, we will look to reduce currency hedging on any further strength.

I HAVE NO ISSUE WITH THE TAXATION OF TRUSTS AS LONG AS THE TAX PAID AT 30% CAN FLOW THROUGH…

Heard nothing about non business assets. Assuming they are just going to strand these assets by moving the goal posts.…

If this was in when I started I would be gone by now. Even now, the 2024 FY is nearly…

So every time you expand this you inadvertently expand the cost of the CLSR which is already unsustainable and unaffordable…

Spot On, Phil's high horse hey