Rumours of 60/40 death exaggerated

Contrary to rumours of its death, the 60/40 portfolio lives on in suitably evolved form, a recent webinar conducted by the Institute of Managed Accounts Professionals (IMAP) has been told.

Betashares Head of Fixed Income, Chamath De Silva made clear that despite persistent narratives in the market, fixed interest remains a relevant as a diversifier.

The webinar involved De Silva alongside Cameron Harrison portfolio manager and partner, Tristan Bowman with JANA Investment Advisers senior consultant, Khurram Jan moderating around the question of whether the old investment playbook, involving 60/40, has stopped working.

Jan put the question to the pair that, with the rise in correlation between bonds and equities the 60:40 construction was losing its relevance.

De Silva opened with a direct rebuttal of one of the more persistent narratives in markets: that rising correlations between bonds and equities have made traditional fixed income irrelevant as a diversifier.

The correlation, he argued, is not a fixed feature of markets — it varies with the inflation regime. Through most of the 2000s, growth was the dominant macro risk and bonds reliably moved inversely to equities. More recently, inflation has taken over as the primary risk, and the correlation between Australian equities and bonds has shifted from negative to moderately positive. But the key question is not whether correlations have risen, it is whether investors are being compensated for the change.

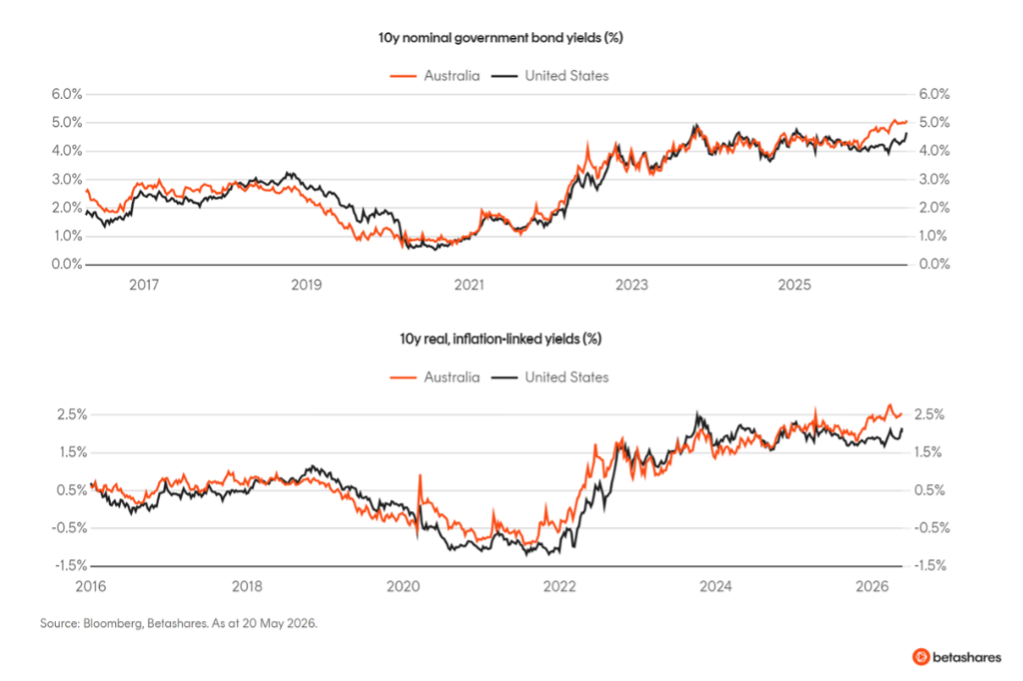

His answer was that they are.

Australian 10-year nominal yields have settled around 5%, while real yields on inflation-linked bonds are at their highest levels since the GFC. The yield curve is upward sloping, with the market pricing a 5-year yield in five years’ time of around 5.5% and a 10-year yield in ten years of close to 6%. Against that backdrop, investment grade bonds in Australian dollars — including state government paper, the major banks and high-quality corporates — are generating income of 5.5 to 6%, which compares favourably with a dividend yield on the ASX 200 that sits below 4%. The 60/40 portfolio is not dead, De Silva concluded; it has simply repriced.

Active Management Is No Longer Optional

Cameron Harrison’s Bowman framed the portfolio construction challenge in terms of separating what fixed income is being asked to do. Inflation-driven volatility has made the equity-bond correlation unstable, and when rates rise sharply it has knock-on effects on bonds, equities, property and infrastructure simultaneously. His response is to disaggregate: treat interest rate duration and credit duration as distinct exposures, manage them actively, and prioritise floating rate securities in portfolios that already carry significant property, growth equity or infrastructure holdings.

Bowman walked through how Cameron Harrison has rotated its credit stack exposure over the past decade — from a large hybrid weighting in 2016 when margins were around 490 basis points over swap, through a high senior debt allocation at the end of COVID, to a deliberate rotation out of Tier 1 hybrids into Tier 2 subordinated debt in 2022 and 2023 when an anomaly saw Tier 2 spreads trade wider than Tier 1. Today, with most fixed income sub-asset classes appearing expensive relative to historical averages, active positioning matters more than ever. The exception he highlighted: senior debt, which remains only slightly below long-run average spreads and continues to benefit from strong offshore demand for Australian credit.

Inflation Protection: The Right Tools, for the Right Investors

Khurram Jan asked what role inflation linked bonds could have in portfolios and both speakers agreed that inflation-linked bonds have rarely looked more theoretically compelling — real yields at 2.5% at the 10-year and close to 3% at 25 years are well above their post-GFC averages. But both were equally candid about the practical constraints. Australian government issuance of inflation-linked bonds has been sparse, with a limited set of maturities and a market where even large institutions worry about their trading footprint. The instrument suits wholesale investors with specific inflation-linked liabilities or long investment horizons, but it is not a straightforward proposition for most retail portfolios, particularly given the sizeable interest rate duration embedded in inflation-linked indices.

For broader inflation protection, De Silva pointed to commodities and commodity-focused equities as the most effective hedge against the kind of unexpected supply shocks that have driven recent inflation episodes — precisely because they reflect physical supply and demand in real time, with minimal duration. The overarching message from both speakers was that fixed income is not a single passive exposure to be set and forgotten. It is a spectrum of instruments with different risk, income, liquidity and inflation characteristics, and matching those characteristics to each client’s specific objectives — investment horizon, risk appetite, income needs and inflation sensitivity — is the real work of portfolio construction in the current environment.

Click here to gain CPD Points

If this does happen it will represent the biggest case of intergenerational theft ever. Older/pension members getting their balances artificially…

Didn't AusSuper lose over a Billion dollars in a failed investment in Plurasight?

There would be NO advice "vacuum" if the insane levels of red tape were removed. This conversation is utter nonsense.…

It is absolute rubbish to link industry fund conflicted advice with the prevention of fraud like Shield.

The Industry Funds want to create a situation where the product provider is able to isolate the advice process so…