ASIC Report spotlights advisers on super switching

The Australian Securities and Investments Commission (ASIC) has made clear in its new REP 833 that it regards financial advisers as central players in superannuation switching particularly where platforms and self-managed funds are concerned.

The regulator made this clear via the following explanation under the heading of “What are inappropriate switching business models?”

ASIC wrote:

“ASIC has long called for superannuation trustees to engage with their members to help them become more confident and make informed choices about the right superannuation fund for them. This can – and should – result in members switching to account types or funds that better suit their needs.

“In contrast to these healthy consumer choices, ASIC is concerned about ‘inappropriate superannuation switching’, whereby people are encouraged or pressured by an adviser to switch their superannuation balance from an existing fund into a different fund or a self-managed superannuation fund (SMSF) for little to no benefit to themselves.

“In these cases, the member’s superannuation is sometimes invested in a platform product, where it may be easier for advisers to charge excessive advice fees, leading to balance erosion. Sometimes, advisers purchase ‘leads’ from firms engaging in lead generation. These lead generators facilitate advisers by targeting a large number of members and conducting a significant proportion of advice on their behalf, despite frequently not being licensed to do so. These models often result in members receiving ‘cookie-cutter’ advice that does not consider their individual objectives, financial situation and needs.

“In the most egregious examples, advisers may recommend investments that are unnecessarily high-risk, illiquid or complex. These models can lead to significant consumer harm, including losses to retirement savings. The Shield and First Guardian matters were examples of this. We are also concerned about cases where the superannuation products recommended are less risky, but the advice provided is inappropriate, unnecessary or overly expensive, and the fees lead to balance erosion.”

Speaking for its platform superannuation constituency, the Financial Services Council (FSC) made clear that they had already moved to address the regulator’s concerns including via adherence to a new Standard to come into effect from 1 July.

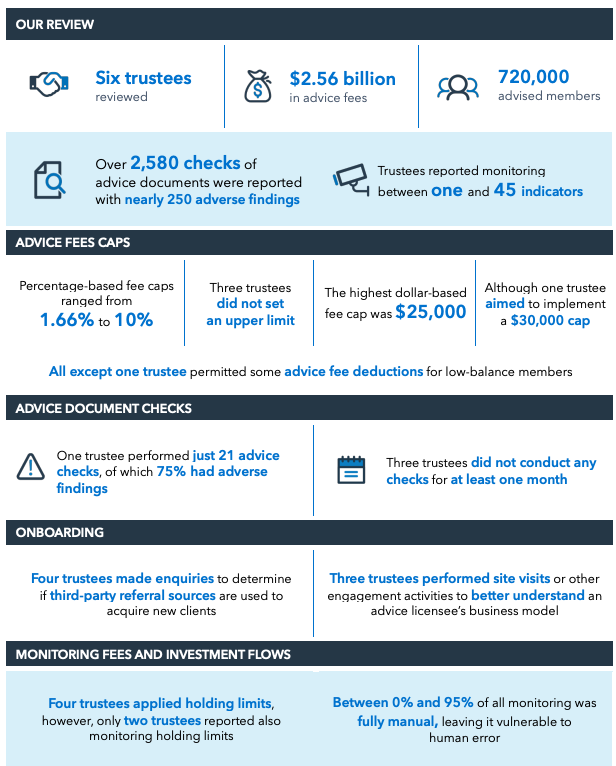

Outlining the review which gave rise to REP833 ASIC said it had reviewed six trustees, $2.56 billion in advice fees and 720,000 advised members.

It then expressed the following as the key issues which concerned it:

- Gaps in advice fee cap controls. With few exceptions, advice fee caps were too high and poorly designed. The highest dollar-based advice fee cap reported was $25,000. Concerningly, one trustee was planning to implement an even higher fee cap of $30,000, which is more than the highest cap of $20,000 identified in REP 781. Some percentage-based fee caps or thresholds were also too high, and three trustees did not have an upper dollar-based limit on what could be charged. This approach can enable very high deductions against larger balances.

- Poor low-balance member protections. One trustee required a $20,000 minimum balance before an advice fee could be deducted, and another implemented additional protection for all account balances below $100,000. The remaining trustees failed to adequately protect low-balance accounts from balance erosion. › Limited checks of advice documents. With few exceptions, trustees did not perform enough checks, and some did not follow up when they had high rates of adverse findings. Three trustees did not conduct any checks for at least one of the months in our review period.

- Not enough focus on business models during onboarding. While trustees do conduct onboarding due diligence of advisers and advice licensees, there was insufficient focus on advice licensees’ business models, including whether they use lead generators or other third-party referral sources.

- Inadequate monitoring of advisers, advice fees and investment flows. Trustees reported inadequate oversight of key risk indicators, such as holding limits, which were only monitored by two trustees in our sample. Trustees also paid insufficient attention to member churn, patterns in fees, and unusual fund flows. Watchlists were widely used, but some lacked clear triggers for escalation or action. Complaints data was also underused. Some trustees over-relied on staff discretion and manual processes, which increased the risk and incidence of human error. Most trustees reported monitoring a large number of red flags and indicators. However, some trustees were narrowly focused on specific topics, such as anti-money laundering or counter-terrorism financing issues, which are important monitoring controls but less helpful in monitoring for inappropriate switching business models or excessive advice fees.

ASIC's real strength is writing a report and then finding research findings to support what they wrote based upon their…

ALP, Unions and Industry Super Funds are that far into each other's pockets it would criminal if anyone bothered looking.…

Isn’t that interesting. Soon after their Labour Party mates shut down the transfer to SMSFs for purchasing property, now they…

The good old ACTU mafia are back in town. The criminal arm of the Labour Party with their bookie mates…

These Government clowns can't do their own job but want more and more involvement in our lives. Just go away…