Discerning the differences in private credit labelling

Negative perceptions of Private Credit are being driven, in part, by the manner in which sponsor-backed direct lending is being mislabelled, an Institute of Managed Accounts Professionals (IMAP) webinar has heard.

The webinar saw MA Financial Head of Global Credit Solutions, Frank Danieli arguing that “private credit” as a term has come to mean something far too narrow.

He stated that what began as a genuine effort to find lending opportunities where banks were no longer the efficient provider of capital – driven by regulation, market structure shifts, or borrower needs around speed and flexibility – has, in practice, often collapsed into a single activity: providing loans to help private equity firms buy companies.

The webinar participants were Danielli, and Australian Ethic’s Adam Roberts, with the moderator being JANA’s Robert Moore.

Danielli acknowledged that sponsor-backed direct lending (lending to companies owned by private equity) is a legitimate part of the credit universe, but Danielli’s data put it in perspective: it represents around 10–15% of total private sector debt, yet accounts for 100% of the mandates of many funds operating under the “private credit” banner.

The consequences of this concentration are now playing out visibly. When managers are set up to do only one thing, competitive pressure forces a familiar sequence: first they give up pricing (spread compression), then covenants, then structural protections. The result, in some corners of the global market, is 85% covenant-light lending, and a heavy concentration in software and technology borrowers — a cohort that is now under scrutiny as AI disrupts the recurring revenue models that made them appear so creditworthy. The problem, Danielli was careful to note, is not lending to tech. It is the concentration that results from fishing in too small a pond – lending to one type of borrower.

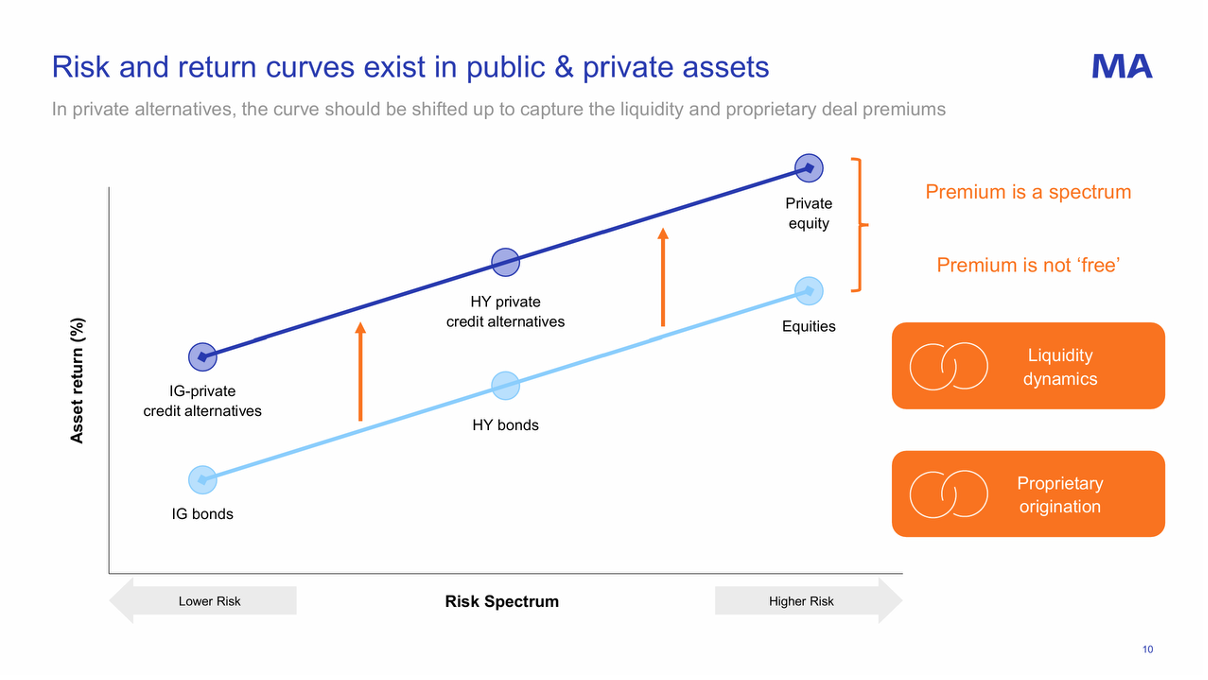

His prescription was direct: advisers need to understand that private credit is a spectrum — investment grade, high yield, and opportunistic — just as traditional fixed income is understood. The return premium relative to traditional fixed income should reflect genuine illiquidity and proprietary deal access, not leverage or risk-taking dressed up as alpha.

Rather than being a single point on the return / volatility curve, each type of private credit offers the potential for its own premium relative to equivalent public market investment types.

Infrastructure Debt: The Quiet Achiever

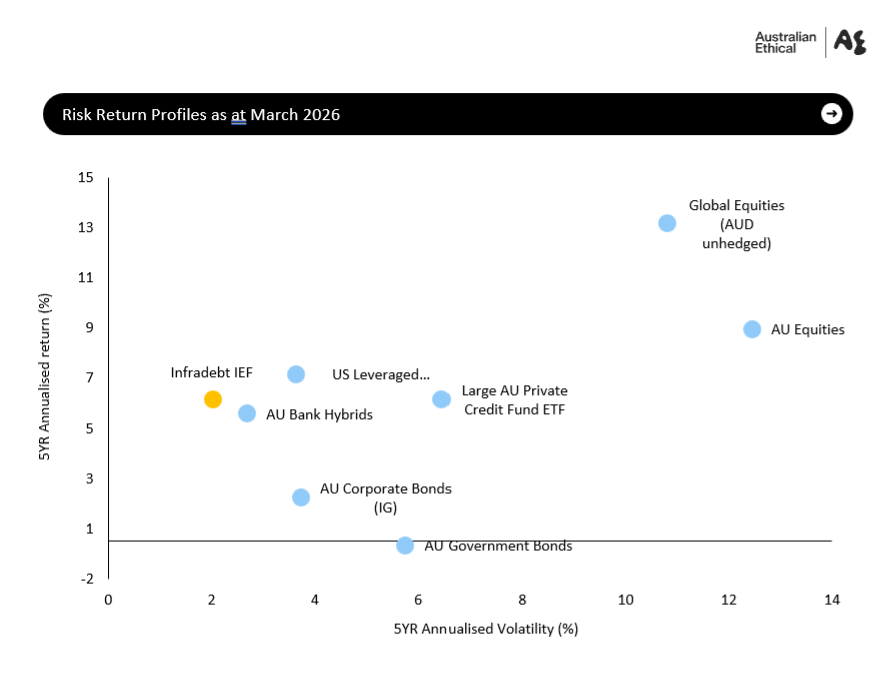

Roberts offered a contrasting perspective — a sector that has largely avoided the headlines, precisely because its fundamentals are harder to overextend. Infrastructure debt, as Australian Ethical approaches it, means senior secured lending against specific projects: renewables, social infrastructure, and asset-backed property with infrastructure-like cash flow characteristics. The appeal is structural. These assets generate high, predictable cash flows, they often carry implicit or explicit government support, and they amortise debt steadily rather than relying on a terminal refinancing event. Default rates, particularly past years two and three of a loan, are historically very low.

The energy transition is the dominant near-term driver of deal flow. Australia has reached roughly 50% renewable penetration in its energy mix, but the targets call for 80% or more by 2030. The first half of the transition, Roberts observed, was the easier half — the lowest-cost projects first. Getting from here to 80% will cost roughly double what has been spent so far: approximately $80 billion in new capital, of which around $40 billion will be debt. With major banks often unwilling to lend below $200–300 million, the mid-market opportunity to lend in this market is wide open, and returns of 300 basis points or more above the cash rate — delivering total returns in the high single digits — are available for well-structured senior secured positions.

AI, Data Centres, and the Limits of Enthusiasm

The presentation closed on the question that is exercising every infrastructure investor right now: the collision of the AI boom with an already-strained energy grid. Roberts’ view was measured. The opportunity is real — data centres anchored to hyperscaler tenants, with pre-committed lease agreements, proper build approvals, and short-dated amortising debt structures, can be excellent lending propositions. But the risks of speculation are equally real: a data centre built without tenants, in a secondary location, funded with long-dated debt, is a very different proposition. The guardrails matter. So does the broader social risk: if finite grid capacity is absorbed by data centres willing to pay premium prices, the regulatory and political blowback on households could reshape the investment landscape quickly.

Unregulated MISs the base problem. Yet MIS remain out of CSLR ? And MIS remain largely Unregulated. WTF Corrupt Canberra

Exactly

Useless ASIC writes another report about excessive breach reporting where ASIC admit mass complaints about a crap crazy Red Tape…

MIS remain the biggest blow ups and impact on CSLR. Yet Mulino still refuses to include MIS directly in CSLR.…

“ remove the traditional cost and access barriers to advice” NGS say. Lies, lies and more Lies. The cost is…