Surviving the economic pressure test

According to Russell Investments’ mid-year outlook, investors have seen markets repeatedly pressure tested by geopolitical tensions, policy uncertainty, and shifting economic expectations over the past six months. Yet the underlying foundations of the global economy have remained intact. While the conflict with Iran tested markets, the S&P 500 recovered its initial decline in less than three months and went on to reach new highs.

Record corporate earnings, improving manufacturing activity, a labor market that remains healthy, and early signs of AI-driven productivity support our constructive view on growth, even as we remain attentive to evolving risks.

In our Mid-Year Outlook, we examine these forces driving market resilience and the key watchpoints we believe will shape markets through the remainder of 2026.

Supercharged global earnings

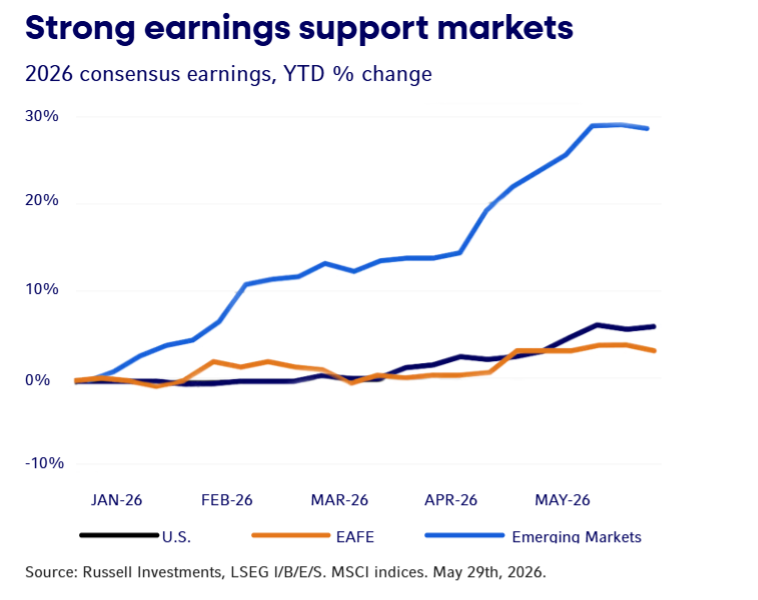

Despite geopolitical pressure, the current supercycle for corporate profits is pushing global equities to new all-time highs. Over the past three years, S&P 500 forward earnings compounded roughly 16% annually—a pace exceeded only by post-recession rebounds in recent decades.

Yet, while earnings have remained strong, leadership has narrowed again after the onset of the Iran conflict. Price and fundamental momentum rotated back to the artificial intelligence (AI) theme—most notably among the tech heavyweights in South Korea and Taiwan. Strong corporate earnings have also helped set the stage for mega-cap IPOs and increased private market activity over the next six months.

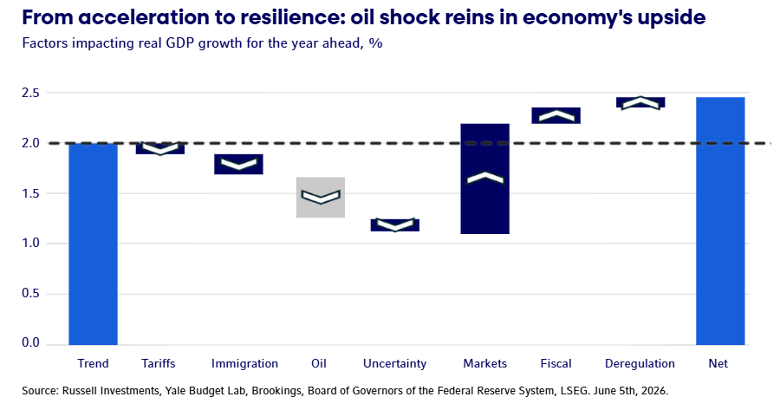

From accelerating growth, back to resilience

The strong global market has largely been underpinned by U.S. growth. In our annual outlook we saw potential for the U.S. economy to inflect from resilience to acceleration, with tailwinds from fiscal stimulus, the AI buildout, and loose financial conditions. Six months later, higher gasoline prices are likely to rein in some of this upside potential.

Despite the pressure, we see a strong U.S. economy and encouraging progress in two areas:

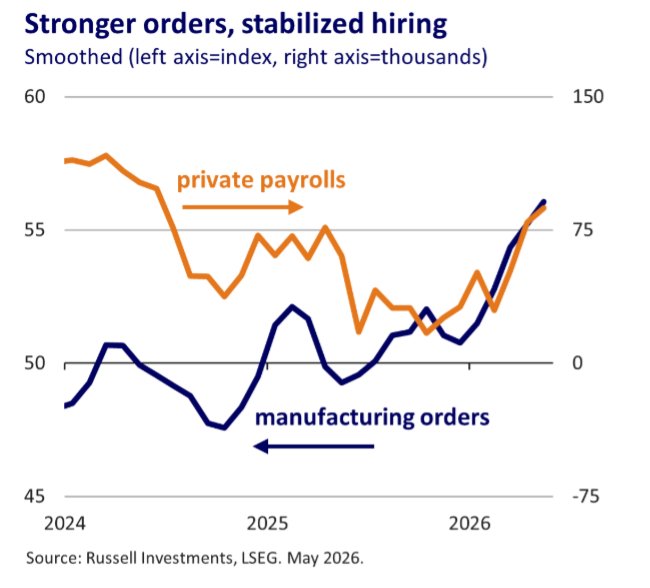

- Manufacturing activity is improving. After years of stagnation, we expect the sector to recover on favorable capex provisions from the One Big Beautiful Bill Act and robust data center demand. Industrial production and the order books for manufacturers are on an uptrend.

- Labor market conditions have stabilized. Private sector hiring slowed sharply in 2025, but our analysis suggested that more than 80% of the slowdown reflected public policy uncertainty rather than private sector distress. For the first half of this year, layoffs remained low and payrolls stabilized at healthier levels in recent months. Job growth also improved. Despite growing concerns about AI’s impact on employment, we continue to see stronger evidence of productivity gains rather than broad-based labor market disruption. So far, the effects appear concentrated in early-career hiring rather than widespread job displacement.

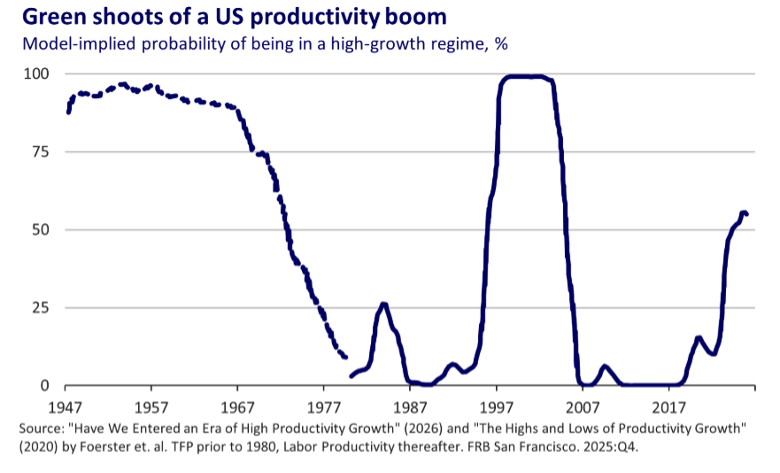

AI shows productivity benefits

Another core pillar of our constructive annual outlook for 2026 was the potential for generative AI to move up the productivity J-curve, bringing more tangible benefits for corporates. While this is likely to be a multi-year theme, six months into 2026 we continue to see encouraging signs of its impact on productivity. Frontier models are increasingly capable, end-user demand for generative AI is strong, and there are green shoots of a new productivity cycle in the macro and microeconomic data.

Economic pressure watchpoints

Halfway through 2026 and the economy remains on solid footing, though several key watchpoints lie ahead.

Watchpoint 1: Cyclical and structural implications of the Iran conflict

While the S&P 500 recovered its initial drawdown from the Iran conflict in just 45 days, the durability of the announced deal and how long commodity flows remain impaired will help shape the rest of the year. When evaluating the risk posed, the distinction between market reactions and fundamental economic impacts remains important. The impact arising from the conflict is likely to filter through commodities, supply chains and inflation, and ultimately, growth.

Mitigating circumstances

Markets are pricing higher inflation risks from the Iran conflict alongside stable growth. So far, we see a combination of structural and cyclical forces as mitigators of the impact on economic activity:

- The global economy not being as exposed to oil shocks as it was in the 70s and 80s. The energy intensity of output and the wallet share of energy in consumption have both declined markedly.

- Oil inventories have been drawn down and consumer demand has rotated to less energy-intensive activities.

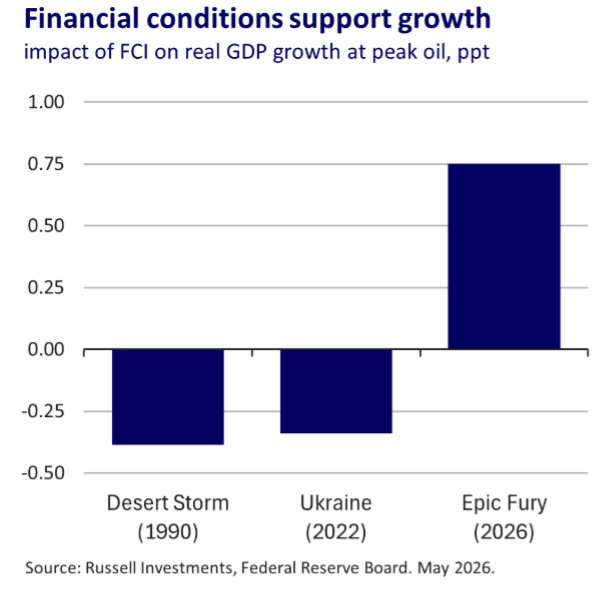

- Larger U.S. tax rebates from 2025 more than offset the hit to U.S. purchasing power this spring.

- “Financial accelerators” are not kicking in. In stark contrast to past major oil shocks, equity and home prices remain near all-time highs and credit spreads are tight.

Even in Europe, the economic drag, while real, could be less severe than 2022. Electricity prices remain well behaved across the continent due to robust wind and solar power generation. Moreover, leading economic indicators point to positive, albeit low gear, growth.

Risk remain

In an adverse re-intensification scenario, the economic effects of the conflict could become more pronounced in the second half of the year as fiscal support fades in the U.S. and inventories are drawn down globally. India may prove to be an important test given the country’s scale and energy dependence on the Middle East.

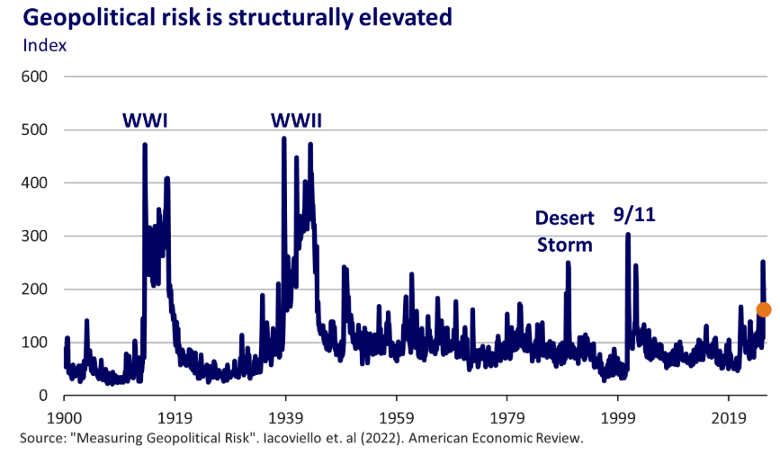

The Iran conflict could also have longer-term implications, particularly after a staccato of geopolitical shocks in recent years. Ramifications include more inflation volatility, higher stock-bond correlations, higher term premia, and a ramp in military spending, with consequences for portfolio diversification and opportunities across public and private markets.

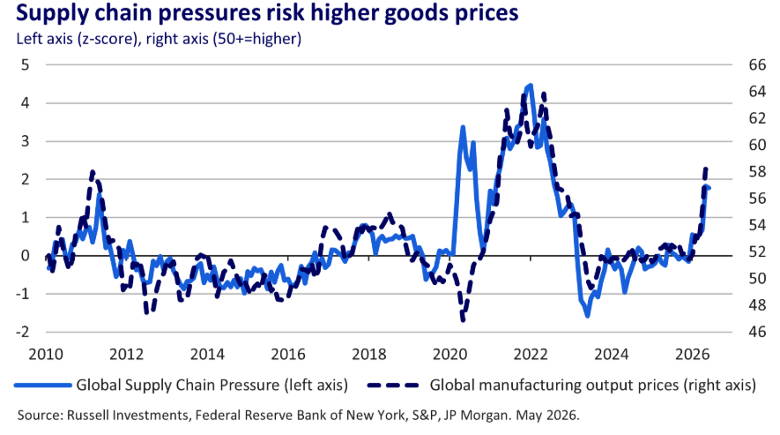

Watchpoint 2: Supply chains strain

The biggest yellow flag facing markets are the signs of emerging supply chain pressures. The Federal Reserve Bank of New York’s Global Supply Chain Pressures Index has spiked to its highest level since 2022. Similar disruptions from the COVID lockdowns contributed to the last inflation surge, and global manufacturers are raising goods prices at a relatively rapid pace again.

Watchpoint 3: Interest-rate volatility

The prospect of rising inflation has led market expectations for policy rates to swing sharply, pivoting from rate cuts to hikes at the onset of the Iran conflict. Our outlook for the Federal Reserve has been more consistent in favoring a protracted hold. While higher energy prices could lift headline inflation, the Fed remains focused on labor market conditions and underlying inflation. On these measures, the backdrop looks more benign. Inflation expectations are well anchored, shelter inflation continues to moderate, and wage growth is consistent with a balanced labor market.

The sharp rise in yields has reshaped the valuation of U.S. Treasuries. Whereas we viewed the front end of the yield curve as expensive at the start of 2026, two-year Treasuries now offer more compelling value. In Europe, inflation plays an even bigger role in monetary policy decisions and we expect hikes from the Bank of England and European Central Bank. Globally, we see good value in several developed market sovereign bonds, including UK Gilts and Japanese government bonds, where investors have priced in higher policy and political risk premia in recent months.

Investor implications

If the first half of 2026 has reinforced one lesson, it is that markets are more resilient than many anticipate. New sources of friction have emerged, including geopolitical tensions, supply chain pressures, and heightened interest-rate volatility, increasing the complexity of the risks facing investors.

Yet resilience has prevailed. Strong market fundamentals continue to support a constructive outlook. For investors, this environment reinforces the importance of maintaining portfolio durability through market regimes, balancing participation in growth opportunities with the diversification needed to withstand periods of stress.

Halfway through the year, the good news is that markets appear to have passed the pressure test. Now the focus is on sustaining it.

Regional Snapshots

United States

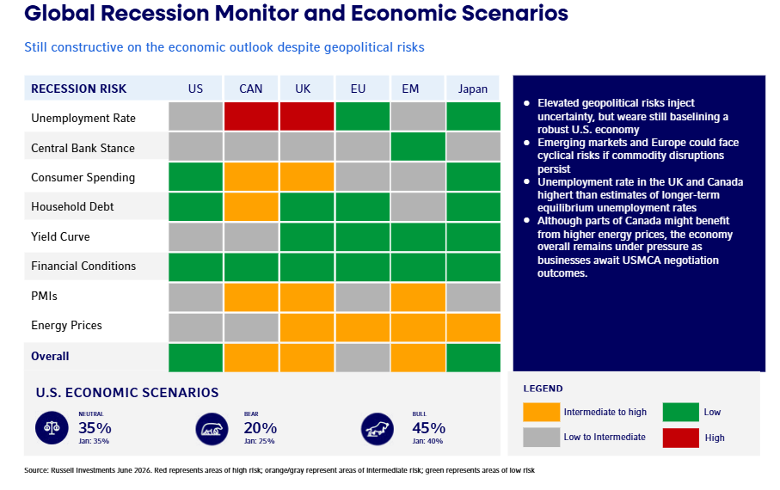

The U.S. economy remains resilient, though its upside potential has moderated as higher energy prices and supply chain pressures complicate the outlook. We look for real GDP growth to hold above 2%, supported by improving manufacturing activity and labor market conditions, the AI buildout, loose financial conditions and fiscal policy. Corporate earnings are supercharged, helping markets advance, though price and fundamental leadership has narrowed back toward the AI theme. We continue to see encouraging signs that generative AI is moving up the productivity J-curve, with potential benefits for company revenues and profit margins over time. The Federal Reserve is likely to remain on hold as higher headline inflation is balanced against anchored inflation expectations, moderating shelter inflation and benign wage inflation. Risks include a protracted Iran conflict, interest-rate volatility and expensive valuations.

Canada

2026 so far has offered investors a reminder that Canada’s economy can look very different from its stock market. Despite the economy having entered a technical recession, Canadian equities are trading near their all-time highs, driven in part by higher energy prices. Earnings continue to hold up, as many Canadian companies derive a substantial portion of their profits from countries like the U.S., which have seen greater economic resilience. For the remainder of the year, we expect the Canadian economy to remain under pressure but remain more constructive on the financial markets.

Eurozone

After the war in the Middle East broke out, we scaled back our exposure to European stocks to neutral. As an energy importer, the eurozone was seen as susceptible to the energy price shock caused by the closure of the Strait of Hormuz. Another headwind for the economy and markets emerged as the ECB raised rates by 25 basis points in June and is expected to follow up with at least one more hike by the end of the year. By contrast, fiscal stimulus through 2026/27 and improving fundamentals for European corporates provide a positive counterweight. The recent agreement between the US and Iran to re-open the Strait of Hormuz, if sustained, could remove the headwinds faced by euro area stocks during the conflict.

United Kingdom

Compared to the start of 2026, events in the Middle East have flipped the outlook for inflation and interest rates in the UK. From previously pricing rate cuts, money markets now expect the Bank of England to raise rates at least once by the end of the year. Like its European neighbours, the UK was seen as vulnerable to the energy supply shock, which now is likely to recede with the re-opening of the Strait of Hormuz. In addition, long-term UK gilts have embedded a significant risk premium due to the uncertainty around Prime Minister Starmer’s position and the fiscal outlook. As underlying economic growth is weak, we think that rate hike expectations are overdone, and gilts offer decent value despite the political unrest.

China

The second half of 2026 is likely to see a pick-up in government stimulus aimed at infrastructure investment, especially if the Middle East conflict extends. The consumer remains fairly subdued, with modest wage growth and lingering concerns about the state of the housing market. Despite this backdrop, we believe Chinese equities still offer good opportunities given cheap valuations and corporate earnings that look healthier than the economic backdrop.

Japan

We believe that Japanese equities look attractive, driven by a combination of corporate governance reforms and potential expansionary fiscal policy from Prime Minister Takaichi’s recent election win. A high stockpile of oil has meant that Japan has proven resilient to the increase in oil prices, but this remains a key watchpoint. The Bank of Japan are likely to raise interest rates once or twice over the next twelve months, while the Japanese yen remains one of the cheapest currencies in the G10.

Hong Kong

Hong Kong economic activity has been responding to the reduction in interest rates, while demand for exports has remained healthy. The property market is a key watchpoint, with early signs that it might have inflected back into positive territory – which could further improve consumer confidence and spending.

Singapore

We expect Singaporean growth to be robust over the next twelve months, with the Middle East tensions a key watchpoint. Singapore has not offered fuel subsidies like many other Asian economies, and historically we have seen oil prices impact the economy with a longer lag than the rest of Asia. Whilst the Monetary Authority of Singapore tightened policy slightly in April, we expect the hurdle for further tightening is quite high.

Taiwan

The Taiwanese economy continues to see significant support from the demand for semiconductor chips, while domestic demand has been improving through the first half of 2026. The Taiwanese equity market has begun to look expensive relative to other Emerging Markets, and we have observed a substantial increase in leveraged activity in the market given the excitement around AI and the demand for chips.

Australia and New Zealand

We are looking at a sub-trend growth environment for the rest of 2026 and into 2027 for the Australian economy. Consumer spending and confidence has fallen following the increase in interest rates from the Reserve Bank of Australia. Productivity remains a challenge for the economy, with the Reserve Bank reiterating its view that economic growth is effectively being constrained at 2%. As a result, corporate earnings are likely to look lackluster compared to global earnings. We believe government bonds in Australia still offer good value, while the Australian dollar is now close to our estimate of fair value.

The key focus for the New Zealand economy in the second half of 2026 will be monetary policy, given the Reserve Bank of New Zealand’s hawkish tilt at the May meeting. The economy is still experiencing tepid growth, inflation is not that far away from target and unemployment is relatively high, so an aggressive shift to interest rate hikes could risk a further step down in the economic situation. Equities appear expensive relative to global equities, while government bonds offer an attractive skew.

CFP grandfathered or not is worth nothing, it is simply a revenue raising exercise by the FAAA. Get your Masters…

Sharpe did some good things while FPA/FAAA chair. Unfortunately his legacy will be tainted by his strident opposition to fixing…

SCA is a joke. I don't know really any effective outcome they've delivered to Australian consumers other than driving up…

Unbelievably low penalty for doing the wrong thing 9.5 million times over 10 years. Advisers have lost their livelihood for…

While we all know super fund call centres can be pretty poor, I wouldn't put too much weight on any…