Traditional active management a ‘zero sum game’

Research and ratings house Morningstar has again pointed to the challenges facing Australian active fund managers and, at the same time, raised its weighted average cost of capital (WACC) across most of them to around 10%.

Morningstar says it views traditional active management as “close to a zero-sum game, where firms grow primarily by taking share from active competitors rather than consistently outperforming passive alternatives”.

In its second quarter active manager industry pulse report, Morningstar has asserted that active managers warrant higher discount rates and said that its decision to lift the average cost of capital reflected structural headwinds that elevate the long0term risk profile for active managers for listed assets.

“First, substitution risk from passive investments. The proliferation of low-cost index funds and smart-beta products has created a fiercely contested market, making client retention harder,” it said.

“Second, fee compression and mandate losses to better-performing active peers. Heightened institutional trustee scrutiny and a crowded global marketplace have accelerated fee pressure, shortened client retention cycles, and lowered tolerance for underperformance,” Morningstar said.

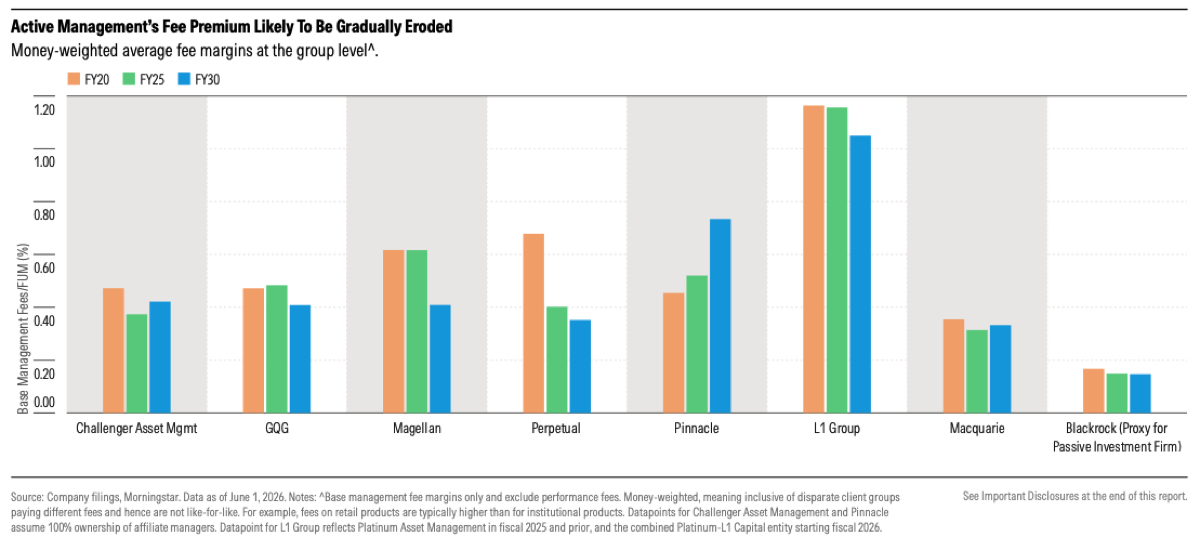

The analysis said that companies were adapting with L1 Group is extracting post-merger cost efficiencies, while Magellan’s stake in Barrenjoey adds a competitive investment banking arm.

“Pinnacle a clearer example still. It continues to capture net flows from weaker peers, underpinned by product diversification, an extensive distribution footprint, and strong investment performance,” Morningstar said.

“Our WACCs for Challenger and Perpetual are unchanged. For Challenger, asset management remains a minor earnings contributor to the broader group, while Perpetual benefits from its more structurally stable corporate trust division,” it said.

The analysis said active managers will likely keep losing market share to passive strategies, many of which are delivered through an ETF structure.

“Passive strategies can deliver market exposure at much lower cost than many active approaches. Within active managers, the pressure falls hardest on conventional equity (such as index-like or long-only) and bond managers, where the strategy is simple enough that passive can do the job. Managers operating in more niche segments—private credit or specialized fixed income—are better positioned to thrive,” it said.

“Active managers continue to cede market share to passive vehicles. Many are burdened by high fees that are hard to justify relative to lacklustre performance. Their response has been to bring active strategies to market through ETFs, but passive ETFs still attract stronger flows—backed by a cost advantage that’s difficult to compete with.

“That pressure to active managers is unlikely to ease—passive giants like Vanguard and BlackRock also offer active strategies of their own, using their scale to crowd the space further.”

People just trusting a "score" was part of the issue... So, maybe let's not force a complicated issue into a…

As per usual this will likely end up as more Red Tape BS.

I am assuming " a requirement to complete online trading" is a typo and should be " a requirement to complete online…

ASIC have ignored property marketers flogging properties to SMSF's for years, this won't change because of the budget. All of…

FAAAAAAAAAAAAAAAAA sound like an ISF mouthpiece. ASIC need to stop SMSF Property spruikers, I have handed them a case for…